Irregular Income Budgeting Chart

This post may contain affiliate links. Read our disclosure policy here.

In the time that I’ve been in the workforce, neither me or my hubby have ever had a set income or a yearly salary. We always lived off some kind of irregular income that varied from week to week and made the task of budgeting into a more difficult chore. When I was working through highschool I used the simple envelope system budgeting. One third of my check went to savings, one third for spending and the last third to pay my small amount of bills (cell phone and car insurance). It as so simple and easy! But now there are car loans and internet bills and garbage bills and all kinds of small and random stuff that quite frankly, gives me a headache.

Normal budgeting charts just didn’t work for us. We just couldn’t allot a specific amount for each bill each month when,

- We didn’t know how much income we would be getting.

- We didn’t always know the amount of the bill. (Like electric, ect)

So when we finally sat down to create a real budget that would work for us, here is what we came up with. I’m also including a Budgeting Chart in this post for you to print and be able to use this budget style for yourself!

First things first, print this BUDGETING CHART that we’ve created, you will need it for the next steps!

Start by figuring out the minimum amount that you will make in a month. Put that in the “Estimated Income” section near the top of the page. If you make commissions they should not be included here. If you have a side job selling on Ebay, unless you have a guaranteed income it should not be included here.

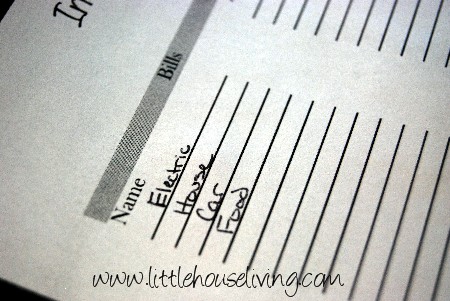

Then start filling out the rows on the left hand side with all of your bills. You may have other things you need to buy and you may want to save money and those are all good things BUT, your bills need to be paid first! Put every single bill you have each month under the Bills section. Don’t put things like “Vacation Fund”. Not a bill. Not going to happen unless you pay your bills. Or unless you want to come home to your electricity being shut off. Up to you. Do put a modest monthly food budget allowance in this section.

*Side note. If your bills total more than your guaranteed income each month, you have a problem. Refer to my Are You Living Beyond Your Means article. You will need to start there instead.

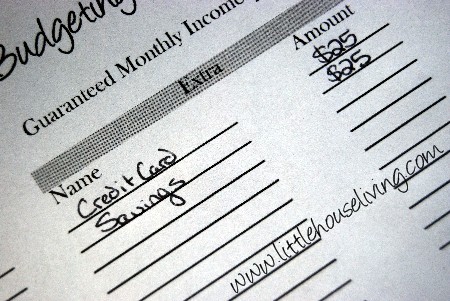

Now go to the other section on the Budgeting Chart that says “Extra”. This is the section where if you happen to have any money left over after bills, you get to do these things. Yay! This section needs to be in order! So for example if you put down:

- Savings – $25

- Food – $25

- Extra Credit Card Payment – $25

- Clothes Savings – $25

- Free Spending – $25

That means that if you make an extra $125 over your regular baseline income, you can put money in savings, have a little extra for food, can make an extra credit card payment, can save to buy some new clothes when you need them, and have some left to spend on yourself. Yay!

This also means that if you have $50 extra beyond your baseline income you can only put $25 in savings and have an extra $25 for food. Make sense? That’s why order in this section is important here. If you really want to pay off that credit card you would put that first. If you really want to build up your savings you will put that first. Go from most important to least important.

See how easy this makes having an irregular income? You know that the bills are going to get paid and then you know exactly where the rest of your check is going to go after the bills get paid. No wasted money, no weird gaps in your budget, all smooth and simple!

Of course don’t forget to print this free BUDGETING CHART to help you figure this all out. And bookmark this page because I promise you will need to make more copies eventually! As debts get paid off you will have to move things around in your “Extra” column to conform to your current needs.

Do you have an irregular income? How do you currently figure out your budget?

This would be really useful for all kinds of people. As a former server, my biggest issue was budgeting a totally unforeseeable amount of money that was never guaranteed. This would have been a big help!

May sound like a dumb question, but would you put tithe and offering on the bills side?

I think it really depends. I know some people would always put it on the bills side no matter what but I feel like if you are barely scratching by then maybe add it to the extras side and find another non-monetary way to contribute your tithe.

I’d like to point out that having bills larger than your minimum income doesn’t *necessarily* mean you’re in trouble – although it might. Our income is very seasonal, so we might make 3x what we need in August, but then be totally out of work the whole month of January. We’re not in trouble, we just have to plan long-term.

I came across your blog via Pinterest and I love it! It was like a rabbit hole, I clicked on a link for …I don’t even remember what now and have been perusing your site for some time now. As a mid-20’s gal, I am trying to find a budget that works for me. I have irregular income and minimal bills but I still feel like I am throwing money away and I’m not exactly sure where it’s going! I have read COUNTLESS articles on budgeting and they are all complex and don’t work for what I need. Yours is simple, straightforward and just what I’ve been looking for. I pay all my bills (besides rent) with a credit card. Your budgeting method plus a couple bits and pieces of other budgeting techniques- cash envelope system for groceries and “fun money”- are going to do the trick! As far as the rest of your site, I have found my go-to for my simple lifestyle project. Thanks again, and wonderful job! (:

Welcome Amanda! I’m glad you found yoru way here 🙂

I’m in the same situation! I never know how much I will bring in each month from my two home businesses, so it’s really hard to budget. Thank you for sharing your budget forms!

Yes, self employment is so hard to budget from! I’m glad this helped!